One of the key indicators that the Central Bank of the Republic of Türkiye (CBRT) takes into account when formulating its monetary policy is the expectations of different sectors. Accordingly, surveys conducted to better understand consumption and saving behavior shaped by economic agents’ expectations serve as a vital source of information. In this blog post, we introduce the Household Expectations Survey (HES), which the CBRT began publishing with the January 2026 data release, and which is designed to measure household expectations in a more comprehensive and robust manner.

An Inflation-Focused Approach

In Türkiye, data on household expectations are compiled through the Consumer Tendency Survey (CTS) conducted by the Turkish Statistical Institute (TURKSTAT). However, as the CTS, implemented in many countries under the coordination of the European Commission, follows a standardized framework, it allows only limited room for revising the questionnaire to include detailed, country-specific questions. Therefore, the CBRT designed the Household Expectations Survey (HES) in a more specific framework, enabling a more comprehensive analysis of households’ expectations regarding inflation and economic and financial indicators closely related to inflation, and their behavioral tendencies consistent with these expectations, and launched it in cooperation with TURKSTAT.

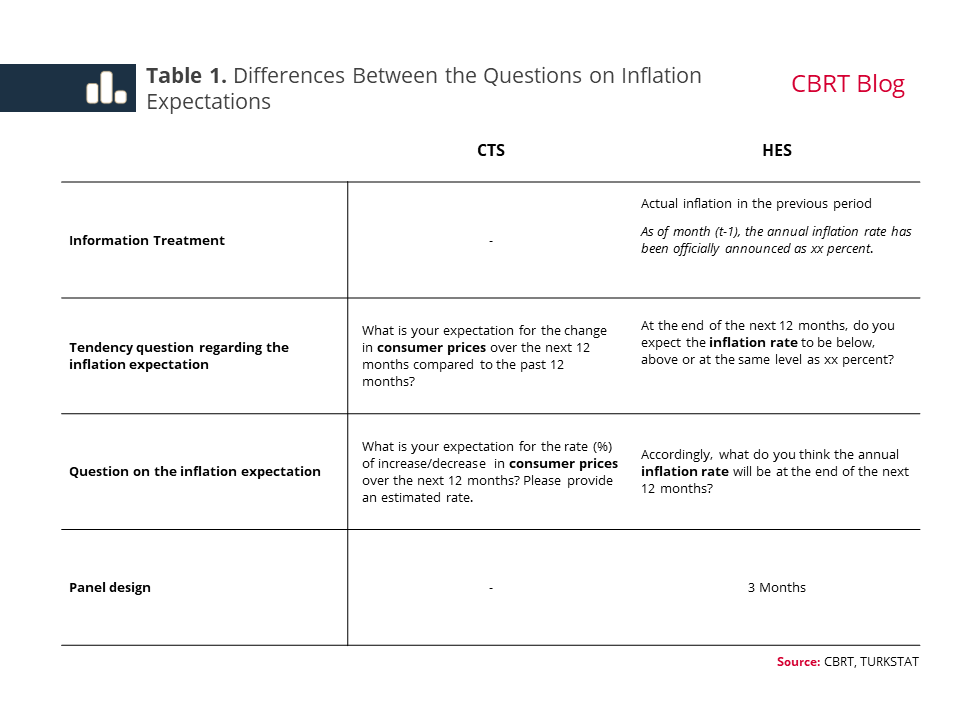

Differences Between the Surveys

The most distinctive feature that differentiates the HES from the CTS is the wording style and the expanded scope of questions on inflation expectations. The phrasing of the questions in the CTS asked to measure households’ inflation expectations may lead participants to interpret them in different ways. The literature also emphasizes that households’ inflation perceptions and expectations are sensitive to the wording of questions. Therefore, in the HES, the question wording has been simplified to refer to the “inflation rate,” providing participants with a clearer and more straightforward framework to allow expectations to be measured accurately. In addition to inflation expectations, the HES also includes questions on households’ assessments and expectations regarding house prices, the US dollar exchange rate and their investment preferences.

One of the innovative features of the HES is that participants are first provided with prior information on the relevant current data and are then asked about their expectations. This approach is referred to information treatment. For example, in the set of questions on inflation, participants are first informed of the annual inflation rate for the previous month. They are then asked to make a comparison with this rate and provide a forward-looking assessment, and subsequently to give an open-ended numerical forecast directly for the inflation rate (Table 1). In this way, the question is made more understandable to the participant, thereby enhancing the internal consistency of expectations and the quality of measurement.

Another methodological advantage of the HES, compared to CTS, is that it is designed as a three-month rotating panel. Under this design, one-third of participants are rotated out of the survey each month and replaced by new participants. This structure makes it possible both to capture new views each month and to track participants over several rounds, thereby enabling the analysis of changes in expectations over time.

In this context, Table 1 summarizes the differences between the questionnaire design and measurement approaches.

Preliminary Findings

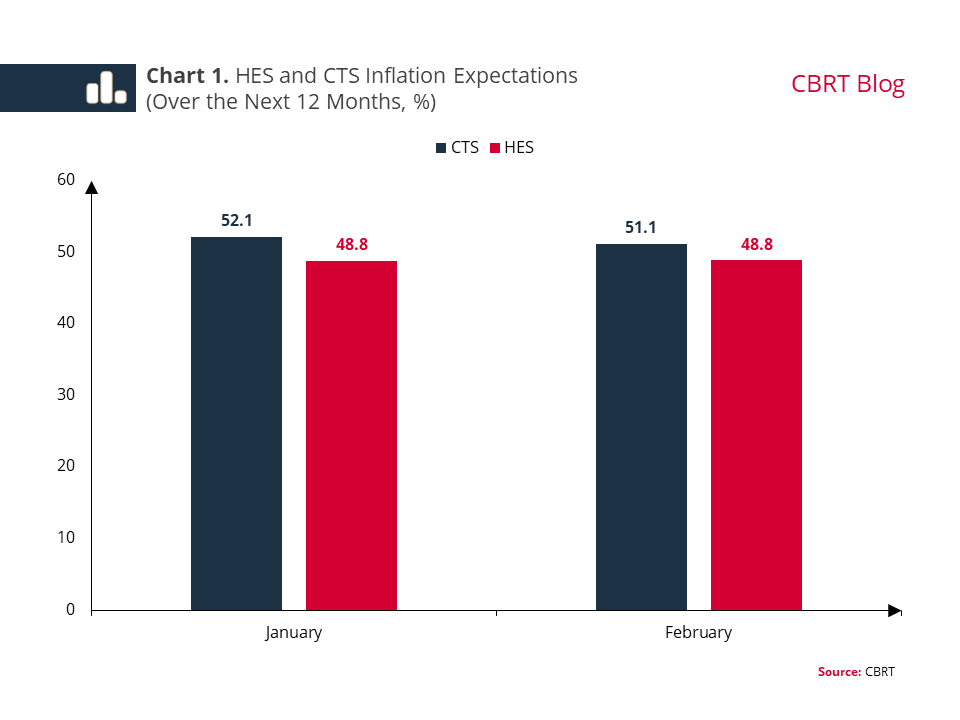

As of the January 2026 data, the HES has replaced the CTS in the calculation of household expectations in the CBRT’s Sectoral Inflation Expectations bulletin. The HES’s question structure, which focuses directly on the consumer inflation rather than the price level, together with the sharing of the previous month’s annual inflation data with participants contribute to the formation of expectations within a clearer reference framework. With the use of the new data source, households’ 12-month-ahead inflation expectations are measured to be 3.3 and 2.3 percentage points lower than those derived from the CTS in January and February, respectively (Chart 1).

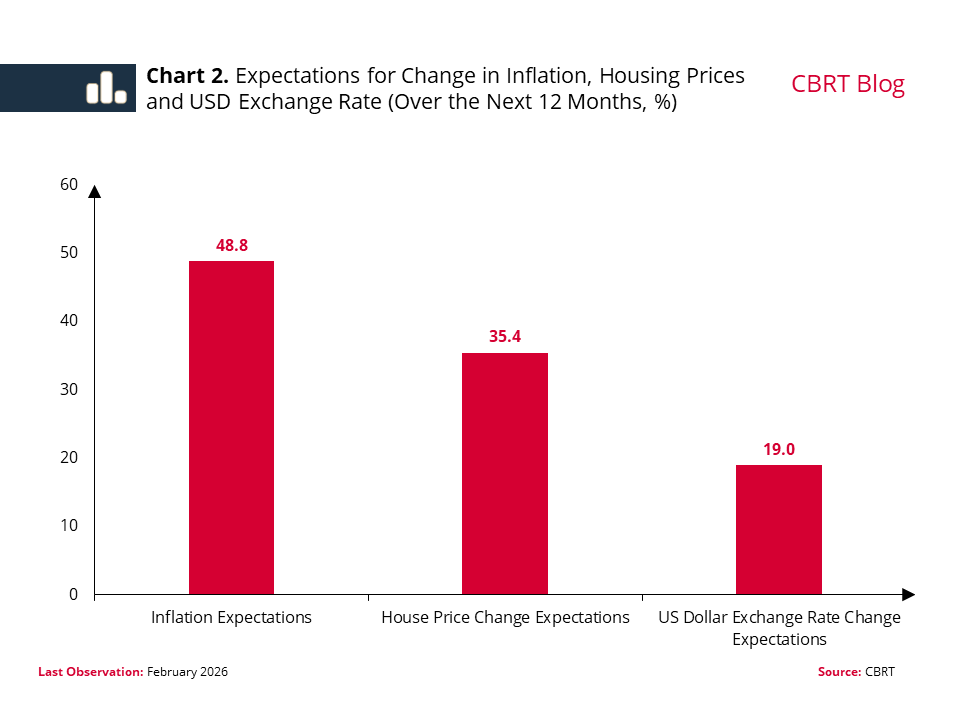

In February, survey participants expect consumer price inflation to be 48.8% and the rise in housing prices to be 35.4% over the next 12 months, while they expect a relatively moderate increase of 19.0% in the USD/TRY exchange rate. The fact that the exchange rate expectations remain below inflation expectations implies that households project a real appreciation of the Turkish lira over this period. On the other hand, the expectation for the increase in housing prices is also below inflation expectations, which points to the expectation of a real decline in housing prices (Chart 2).

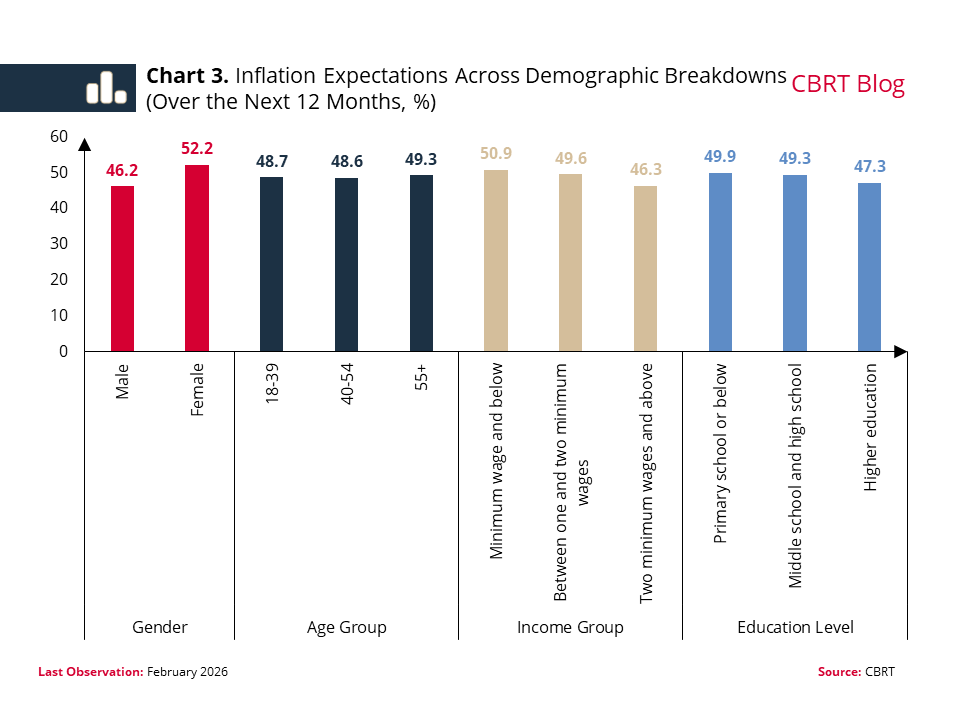

With this new survey, the CBRT publishes the participants’ expectations in demographic breakdowns by gender, age, income and education levels. In February, an analysis of 12-month-ahead inflation expectations across demographic breakdowns reveals that limited differences appear among groups, and expectations cluster around a narrow range (Chart 3).

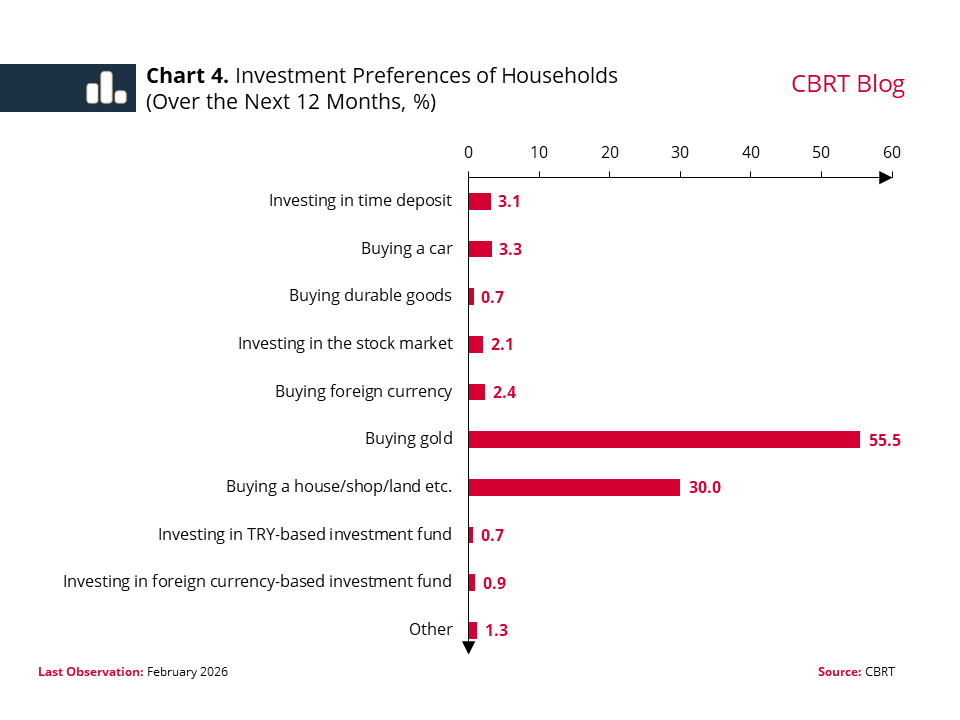

Another new question in the survey is about the investment instrument the participants would prioritize if they currently had cash available for investment, in view of their inflation and exchange rate expectations. The results indicate that households have a strong tendency to opt for traditional investment instruments. In February, 55.5% of the participants ranked gold first among investment instruments, while 30% prioritized real estate. Foreign exchange and other financial instruments appear to be preferred only to a limited extent (Chart 4).

Conclusion

In sum, the HES enables the measurement of households’ expectations in a clearer and comprehensive way with an approach specific to Türkiye, within an inflation-centered framework. With this improvement, as of January 2026, the survey begins to be used in the CBRT’s Sectoral Inflation Expectations bulletin to represent household expectations. With continued tight monetary policy stance and disinflation process, we expect households’ inflation expectations to continue to improve and the gap between expectations and inflation to narrow gradually.